Executive Condominiums matter because they can narrow the gap between public housing affordability and private condo living for Singapore first-time buyers. The main challenge is that an EC is not just a cheaper condo. It comes with eligibility rules, bank loan constraints, grant conditions, and project-specific trade-offs that can affect both monthly cash flow and long-term upside. A smart EC first-timer approach solves one problem well: choosing a launch you can actually qualify for, afford, and hold comfortably through the 5-year Minimum Occupation Period.

What makes an EC a strong first home for a first-timer?

Yes. HDB households and CPF grant-eligible couples often use ECs as a lower-entry path than comparable private condos in Tampines or Bukit Batok.

A new EC from a developer gives first-time buyers a rare mix of subsidy-linked pricing and condo facilities. Eligible first-timers may receive up to S$30,000 in CPF Housing Grants, which can directly reduce the cash and CPF burden at purchase. That matters when every S$50,000 in price can materially change your loan size and monthly instalment.

The trade-off is structure. A new EC is still subject to HDB rules at purchase, even though the development itself looks and functions like a private condo. You get a 5-year MOP (note: w.e.f from new EC land sales from 8 May 2026, the MOP is 10-years) resale restrictions during that period, and no HDB loan option. If you want the lifestyle upside without public-housing conditions, a private condo may fit better. If value matters more than immediate flexibility, ECs are usually the stronger first-home route.

How do you check EC first-timer eligibility step by step?

Start with HDB rules, not showflats. The key gates are Singapore citizenship, a valid family nucleus, and the S$16,000 household income ceiling.

Step 1 is household structure. For a new EC, at least one applicant must be a Singapore Citizen, and you must apply under an accepted scheme such as the Public Scheme or Fiancé/Fiancée Scheme. A common misconception is that any single buyer above 35 can buy a new EC alone. That is not generally true unless the application fits the Joint Singles Scheme.

Step 2 is income and property history. If total gross monthly household income exceeds S$16,000, then you cannot buy a new EC from a developer. If you or your spouse owned private property or disposed of it within the last 30 months, then you will usually be ineligible as well.

Step 3 is current housing status. If you already own an HDB flat, you must meet the relevant HDB conditions and, after key collection for the EC, sell the HDB within the required timeline. Buyers often check eligibility too late, after emotionally committing to a project. That is the wrong order.

How do you calculate EC affordability for a first-time buyer step by step?

Use bank-loan rules first. MAS limits and HDB EC rules mean buyers usually face up to 75% LTV and a 30% MSR.

Step 1 is setting a real budget, not a wish-list budget. Include down payment, Buyer’s Stamp Duty, legal fees, and a renovation buffer. Buyers who focus only on headline launch price often understate total upfront funds by tens of thousands of dollars.

Step 2 is working from MSR. If your household earns S$14,000 a month, then a 30% MSR suggests a ceiling of about S$4,200 for monthly mortgage repayments. Banks also stress-test affordability, so the figure you are comfortable with and the figure the bank approves may not match exactly. An in-principle approval from DBS, UOB, OCBC, or another lender gives a much cleaner range before you visit a showflat.

Step 3 is comparing total quantum, not just psf. A unit at S$1,766 psf can still be more affordable than a cheaper-psf unit if the layout is smaller and more efficient. That is a frequent first-timer mistake. Grant support up to S$30,000 helps, but it does not fix an over-stretched monthly instalment.

What resources help EC first-timers shortlist the right launch in Singapore?

Use live project data, not brochure hype. Executive Condominium Singapore, HDB, and bank IPA channels give the fastest reality check.

Before you compare projects, compare information quality. The best shortlist usually comes from combining official eligibility rules, real-time launch data, and financing checks.

- Executive Condominium Singapore: Live EC pricing, floor plans, availability updates, eligibility screening, affordability guidance, and booking support in one place.

- HDB EC eligibility pages: Official rules on income ceiling, family nucleus, private property restrictions, and first-timer criteria.

- Bank IPA channels from DBS, UOB, or OCBC: Early borrowing range and monthly repayment checks.

- URA Master Plan and OneMap: Confirmed transport links, surrounding land use, and future supply context.

- Developer e-brochures and showflats: Latest stack plans, payment scheme details, and launch-day inventory.

Which EC projects look strongest for first-time buyers in 2025?

Aurelle of Tampines , Otto Place, Novo Place, Lumina Grand, and Coastal Cabana stood out because they combine family-sized layouts, transport access, and EC pricing.

Aurelle of Tampines is the most obvious choice for buyers who want east-side convenience and strong launch momentum. It was reported at about S$1,766 psf on average and achieved roughly 90% sold on launch weekend. Its appeal is simple: upcoming Tampines North MRT, nearby schools, and access to Changi Business Park plus Tampines Regional Centre.

Otto Place suits first-timers who want a more deliberate family layout strategy. Its launch average was reported around S$1,700 psf, and its unit mix is clearer than many EC launches, with 3-bedroom and 4-bedroom layouts from about 872 sqft to 1,195 sqft. If you need a study and expect hybrid work or a growing household, this matters more than a flashy facility deck.

Novo Place is a value-growth play in Tengah. Its reported average of about S$1,654 psf makes it easier to enter than some newer launches, and the project benefits from future Tengah Park MRT connectivity. Lumina Grand pushed value even harder at about S$1,464 psf on launch weekend, which is why it remains relevant for first-timers who prioritise lower entry psf in the west.

Lumina Grand pushed value even harder at about S$1,464 psf on launch weekend, which is why it remains relevant for first-timers who prioritise lower entry psf in the west.

Coastal Cabana was also the one to watch if east-side scarcity is part of your plan. Pasir Ris has not seen a new EC launch in about 12 years, and the appeal is tied to Pasir Ris MRT, the Cross Island Line, Changi Airport Terminal 5 growth, and lifestyle amenities near Downtown East and Pasir Ris Park.

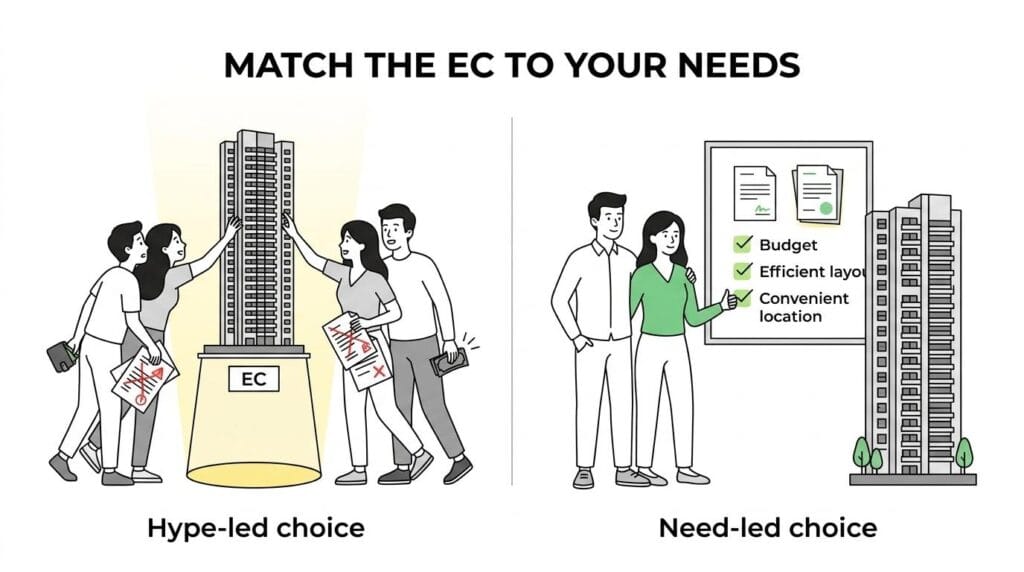

Is a new EC better than a private condo for a first-time buyer?

Usually yes for value, but not for flexibility. A new EC and a private condo in Tampines or Pasir Ris solve different problems.

For many first-time buyers, the EC wins because the pricing gap versus a comparable private condo can be meaningful while facilities remain broadly similar. Yet the restrictions are real, and they shape who should buy what.

- New EC: lower entry pricing, possible CPF grant support, but subject to eligibility rules and 5-year MOP (note: w.e.f from new EC land sales from 8 May 2026, the MOP is 10-years)

- Private condo: no income ceiling or public-housing eligibility gate, but usually higher purchase quantum

- New EC: bank financing only, with MSR and HDB-linked purchase conditions

- Private condo: more immediate flexibility for resale and whole-unit rental, depending on market conditions

A common misconception is that a new EC is simply a discounted private condo. It is not. If you plan to stay put and want stronger value per dollar, the EC is often the better fit.

How do Aurelle of Tampines, Otto Place, Novo Place, and Lumina Grand compare for first-timers?

Aurelle favours east-region convenience, while Otto Place, Novo Place, and Lumina Grand favour west-side growth near Tengah and Jurong.

Choose Aurelle if you want a more mature regional story. Tampines already has strong retail, schools, and employment anchors. The trade-off is price. Its higher average psf means you are paying more for a location with clearer present-day utility.

Choose Otto Place & Novo Place if you value layout depth and future-oriented growth. Tengah is still shaping up, but proximity to the Jurong Region Line, Jurong Innovation District, and Jurong Lake District supports a longer-run upside case. Novo Place makes a similar bet with a slightly lower reported average psf. If your budget is tighter and you can wait for the town to mature, Novo Place can be the cleaner entry point.

Lumina Grand sits in a different lane. It is more affordability-led and benefits from Bukit Batok access plus Tengah adjacency. If your priority is getting into the EC market at a lower entry level, Lumina Grand may be easier to justify than chasing the most popular launch.

How should an EC first-timer move from enquiry to booking step by step?

Treat booking like a sequence, not a weekend decision. IPA approval, document prep, and unit strategy matter more than brochure timing.

Step 1 is financing readiness. Secure your bank IPA and gather documents early, including NRIC, income records, CPF statements, and any HDB ownership documents. If you are buying under the Fiancé/Fiancée Scheme, then marriage timeline documents matter too.

Step 2 is project filtering. Narrow your shortlist by total price, layout fit, and location logic. If one spouse works near Changi and the other needs nearby primary schools, then an east-side project may justify a higher psf. If both prioritise entry cost and can wait for town growth, then a Tengah project may make more sense.

Step 3 is launch execution. Go into the booking window with a first choice, second choice, and a walk-away price. Pro tip: popular stack types can move quickly, especially in launches with strong weekend demand. Buyers who improvise on the day often stretch their budget for a unit they did not originally want.

What hidden costs and rules do EC first-timers often miss?

Stamp duties and timelines matter as much as psf. BSD, legal fees, and the 5-year MOP (note: w.e.f from new EC land sales from 8 May 2026, the MOP is 10-years) can change the real cost of an EC.

A launch price is only part of the bill. First-timers usually plan for the mortgage and renovation, but miss the friction costs around purchase and holding period.

- Buyer’s Stamp Duty

- Legal and conveyancing fees

- Valuation or administrative charges

- Renovation and furniture buffer

- Sale timing obligations for existing HDB owners

Another misconception is about rental flexibility. During the 5-year MOP (note: w.e.f from new EC land sales from 8 May 2026, the MOP is 10-years), you generally cannot sell the EC and cannot rent out the whole unit. Room rental may be allowed subject to the relevant rules. If your plan depends on full-unit rental income soon after key collection, then the EC route does not match your strategy.

Why do MRT access, schools, and growth nodes matter for EC resale value?

Transport and jobs support resale more reliably than lifestyle extras. Tampines North MRT, Changi Business Park, and Jurong Lake District are stronger value drivers than a larger clubhouse.

EC buyers often focus on facilities because those are visible at the showflat. Resale buyers focus more on daily friction. A manageable walk to MRT, practical school access, and job-node connectivity reduce that friction and widen the future buyer pool.

That is why Aurelle of Tampines has a straightforward story. It combines an upcoming MRT with a mature regional ecosystem. Otto Place and Novo Place have a different, but still valid, logic: future Tengah connectivity and west-side employment growth. The trade-off is timing. If infrastructure is still upcoming, then you are paying for future convenience rather than current convenience.

Pro tip: check whether a transport link is operational, under construction, or still at planning stage. Those three situations should not be valued the same way.

What mistakes should EC first-timers avoid before booking?

Most mistakes start before the showflat. HDB rules, bank buffers, and unit efficiency beat impulse buying every time.

The first error is chasing the lowest psf without checking quantum and layout wastage. A cheaper-psf unit can still strain your finances if it is larger than you need. The second is ignoring exit timing. A project may look attractive on resale assumptions, but if you cannot hold it comfortably through MOP, the upside becomes irrelevant.

The third is treating all upcoming locations as equal. Tampines, Tengah, Bukit Batok, and Pasir Ris each have different risk-reward profiles. Some offer stronger current liveability. Others ask for patience in exchange for potential value catch-up.

- Chasing psf only: total price and usable layout matter more

- Ignoring financing buffers: bank approval and personal comfort are not the same

- Underestimating MOP: resale and rental flexibility come later, not immediately

- Booking too slowly: strong launches can compress decision time, so paperwork must be ready

A disciplined EC first-timer wins by filtering hard before falling in love with a unit. That is usually the difference between a confident purchase and a stretched one.

Disclaimer: While reasonable care has been taken in preparing this website, neither the developer nor its appointed agents guarantee the accuracy of the information provided. To the fullest extent permitted by law, the information, statements, and representations on this website should not be considered factual representations, offers, or warranties (explicit or implied) by the developer or its agents. They are not intended to form any part of a contract for the sale of housing units. Please note that visual elements such as images and drawings are artists’ impressions and not factual depictions. The brand, color, and model of all materials, fittings, equipment, finishes, installations, and appliances are subject to the developer’s architect’s selection, market availability, and the developer’s sole discretion. All information on this website is accurate at the time of publication but may change as required by relevant authorities or the developer. The floor areas mentioned are approximate and subject to final survey.